The Internal Revenue Service can charge you penalties and interest if you are late paying your taxes.

The amount you are charged is based on several factors. Interest is easier to calculate than penalties, which depend on additional factors.If you pay your taxes late, the IRS can charge you interest on the unpaid balance and assess a penalty based on how late you are. The exact amount you'll have to pay depends on a few factors.

Those factors include whether you filed your tax return on time, how much you still owe, and the current interest rate, among others. Although the IRS treats each late payment on a case-by-case basis, here's how you can get a good idea of what you'll owe in interest and penalties.

Of the two charges you could face, interest is the more straightforward to calculate. The IRS interest rate is determined by the federal short-term rate plus 3%. Since the current federal short-term annual interest rate is 4.71%, the interest rate charged on late tax payments was 7.71% as of March 2024.

Keep in mind that interest rates fluctuate with time, so this can (and likely will) change over time. Interest is computed on a daily basis, so each day you are late paying your taxes, you'll owe 0.0082% of the balance.

So, if you owe the IRS $1,000, are 90 days late, and the interest rate is approximately 5%, calculate your daily interest charge -- which would be about $0.082 -- and then multiply that by 90 days to arrive at the total interest charge of $7.40.

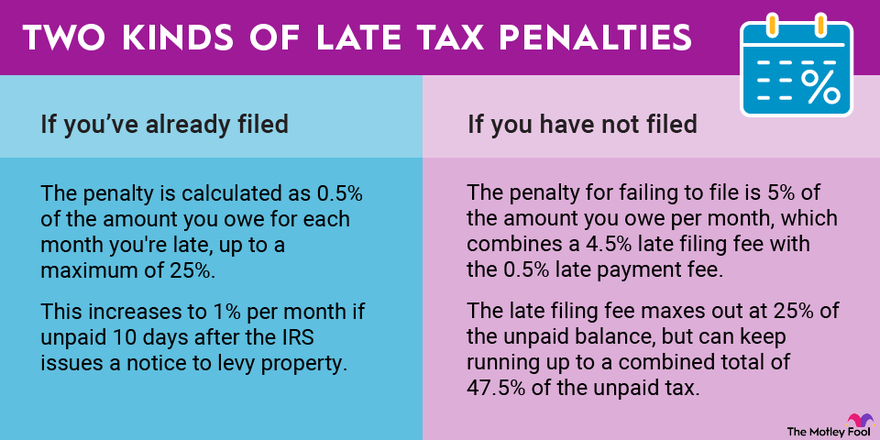

Late penalties can be a bit tougher to calculate and depend on whether you've filed your return. If you owe the IRS a balance, the penalty is calculated as 0.5% of the amount you owe for each month (or partial month) you're late, up to a maximum of 25%. This late penalty increases to 1% per month if your taxes remain unpaid 10 days after the IRS issues a notice to levy property.

On the other hand, if you don't file your tax return on time, the penalty is much more severe. The penalty for failing to file is 5% of the amount you owe per month (or partial month), which combines a 4.5% late filing fee with the 0.5% late payment fee. Now, the late filing fee also maxes out at 25% of the unpaid balance, but the late payment fee can keep running up to a combined total of 47.5% of the unpaid tax.

Finally, if you filed your return more than 60 days late, the minimum penalty for failure to file is $135 or 100% of the tax you owe, whichever is smaller.

As you can see, the monthly penalty for not filing your tax return is 10 times higher than the penalty for paying late. So, if you cannot pay the amount you owe by the filing date, it's important to file your return anyway.

Also, it's important to mention that penalties and interest can be charged even if you file an extension. An extension simply moves the filing deadline from April 15 to Oct. 15. However, if you owe taxes for the year, the amount is still due on April 15. If it's not paid in full by the April 15 deadline, interest and penalties can start accumulating.

Let's consider the case of someone who files their return on time but owes $5,000 and pays the balance 110 days after the April 15 deadline. Based on the daily interest calculation described earlier, this taxpayer would owe $45.21 in interest charges.

And since 110 days is more than three months but less than four, they would have to pay four months' worth of late payment penalties, or 2% of the balance (0.5% times four months). This translates to a late payment penalty of $100. So, interest and penalties add up to $145.21 in this case.

We briefly mentioned that the IRS considers each case individually. What this means is that penalties can be waived or reduced if there is a legitimate reason for not filing or paying taxes. According to the IRS website: "The IRS may abate penalties for filing and paying late if you have reasonable cause and the failure was not due to willful neglect."

Here's how to calculate your take-home pay as a percentage of your gross pay to see how much of your hard-earned money is actually

Everything you need to know to calculate an interest rate with the present value formula.

Form W-9 doesn't usually result in income taxes withheld, but there is an exception.

The net worth of a business is also known as its book value or its owners' (stockholders') equity.

For example, if you were in the hospital for a week leading up to the filing deadline, the IRS may show leniency. Or if you are a victim of a natural disaster, the IRS can choose to waive deadlines. However, in most cases, interest and penalties begin to accumulate on unpaid balances as soon as the April 15 deadline passes.

This article is part of The Motley Fool's Knowledge Center, which was created based on the collected wisdom of a fantastic community of investors. We'd love to hear your questions, thoughts, and opinions on the Knowledge Center in general or this page in particular. Your input will help us help the world invest, better! Email us at [email protected]. Thanks -- and Fool on!